- House prices are predicted to fall by between -2% and -4% in 2024, given the broader economic challenges, and the likelihood that mild downward pressure on house prices continues.

- Pressure on household finances – notably from inflation and higher interest rates – has impacted housing affordability, leading to fewer completions.

- A partial recovery in market confidence and transaction volumes is expected in 2024 as interest rates ease and affordability improves.

- As with recent years, forecast uncertainty remains high given the current economic environment.

Attributable to Kim Kinnaird, Director, Halifax Mortgages:

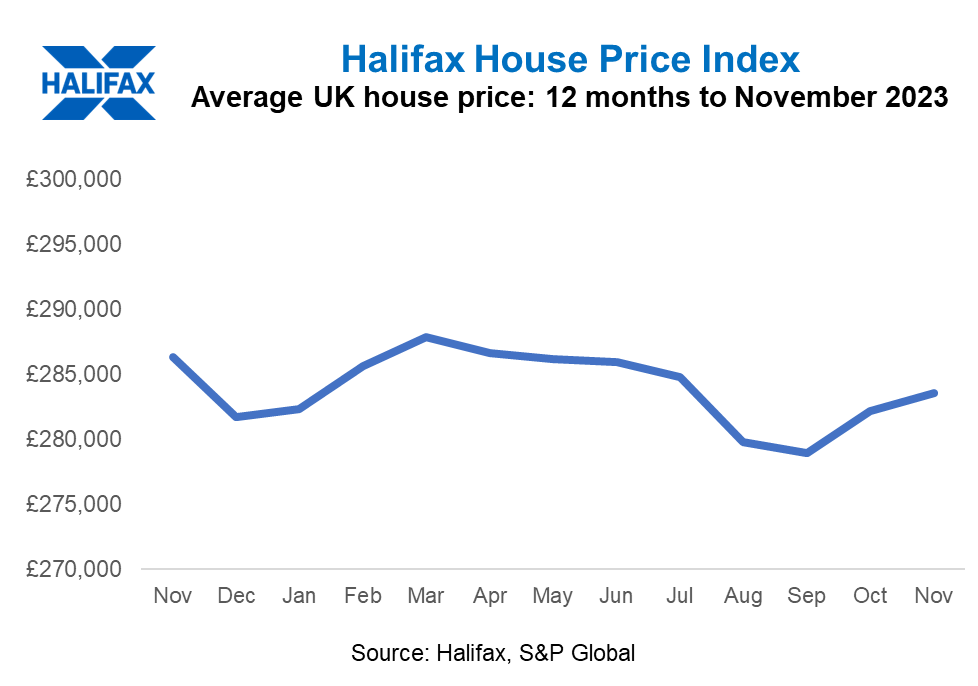

“UK property prices held up better than expected over the last year, falling by just -1.0% on an annual basis, to now sit at £283,615. This resilience – which owes more to the shortage of available properties for sale than strength of demand among buyers – means average house prices end the year just 3% down on August 2022’s peak (£293,025) but £44,000 above pre-pandemic levels.

“To some extent this masks the fluctuations we’ve seen in the housing market throughout 2023. As wider economic headwinds began to bite, house prices fell for six consecutive months between April and September, before rising again later in the year as prospects improved. And it’s a mixed picture across the country too, with some areas still seeing annual growth, such as Northern Ireland at +2.3%, while in regions like the South East of England house prices continued to drop (-5.7%).

“Higher interest rates, and the resulting squeeze on affordability, gave many potential home buyers pause for thought when considering making a move over the last year. Mortgage approvals were down a quarter across the market, while overall housing transactions were a little under 20% down – both the lowest in at least a decade.

“As homeowners were hesitant to move, there was a natural reduction in the stock of available properties. Crucially, with unemployment levels only seeing a marginal increase, and many homeowners protected from the immediate impact of rising interest rates by fixed rate deals, there doesn’t appear to have been a spike in the number of ‘forced sales’ – those who feel compelled to sell but would prefer not to, typically triggered by financial pressures.

“We’ve also seen activity among first time buyers fare relatively well, despite the obvious financial hurdles they face. This could be down to rapidly rising rents – up by over 8% in the year to October. We’ve seen first time buyers adjusting their expectations to enable them to still get on the property ladder, such as buying smaller properties, to compensate for higher borrowing costs.

“The impact of rising mortgage rates has also been partially offset by rapid pay growth, which accelerated to almost 8% across the middle of the year. In comparison to the rise in average pay, the real-term decline in house prices has been around 13% since August 2022, taking the average house price to income ratio down to its lowest since 2015.

“Looking ahead, now that inflation is falling back, financial markets are pricing in cuts to Base Rate during 2024. Mortgage rates are already falling, with a typical 5-year fixed 75% LTV deal now below 5%, having been as high as 5.7% as recently as July. All being equal, these rates are expected to fall further over the coming months.

“However, while pay growth is now above inflation – beginning to ease the cost of living squeeze for some – other factors will continue to weigh on households’ spending power next year. Economic growth is expected to remain weak, with unemployment rising and frozen tax thresholds limiting any increase in take home earnings.

“Overall, with the combination of cost of living pressures and interest rate levels that are still much higher than even two years ago, we will likely see continued mild downward pressure on house prices. Our latest forecast suggests a fall of between -2% and -4% in 2024, though it should be noted, as with recent years, forecast uncertainty remains high given the current economic environment.”

Key facts and figures:

- The average UK house price is now £283,615 compared to £286,328 a year ago, a fall of £2,713.

- Annual house price growth is -1.0% (year to November). During 2023 it was as high as +2.1% (January and February) and as low as -4.5% (August and September).

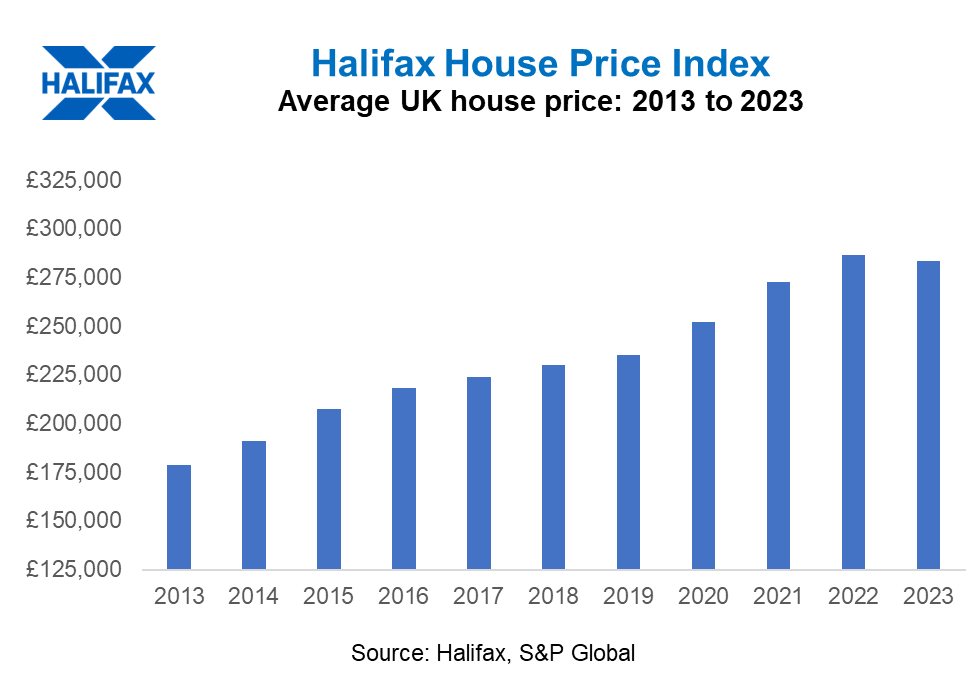

- Average property prices are £44,439 (+18.6%) higher than at the onset of the pandemic (£239,176 in March 2020).

- Property prices for homes bought by first time buyers recorded slight growth (+0.5%) over the last year, while the amount paid by home-movers fell by -1.7%.

- Northern Ireland saw the highest rate of annual property price inflation of any UK region or nation in the year to November 2023 at +2.3%. The South East of England recorded the biggest decrease, down by -5.7%.

- The all-time record high UK average property price was set in August 2022 (£293,025).

- The typical UK house price has increased by +59% over the last decade (£178,501 in November 2013), a rise of £105,114.

Notes:

• 2024 house price forecast based on Lloyds Banking Group’s economic projections as stated in its 2023 Q3 results: https://www.lloydsbankinggroup.com/investors.html

• All house price figures, unless otherwise stated, taken from the Halifax House Price Index up to and including November 2023 data: https://www.halifax.co.uk/media-centre/house-price-index.html

First Time Buyer is an exciting bi-monthly glossy which takes a stylish and comprehensive look at all the options available, setting them out in an entertaining and informative way, and helping potential customers navigate their way through what is often a daunting and complex process. We dispel the myths, reinforce the facts and arm the reader with the tools necessary to make their homeownership dreams a reality.